English

English Français

Français Español

Español Bahasa Indonesia

Bahasa Indonesia 中文 (中国)

中文 (中国) Русский

Русский Português

Português Deutsch

DeutschTable of Contents

When hearing the word ‘cryptocurrency,’ many people immediately think of Bitcoin. And indeed, Bitcoin is the oldest and the most famous of the cryptocurrencies available on the market. But it’s hardly the first digital form of money or even the first blockchain. Let’s dive in and review some history and facts about Cryptocurrencies and other blockchain-based assets.

What is Cryptocurrency?

Banks offer a digital version of fiat money. We encounter them every time we transfer money or pay by card, but those are not considered cryptocurrency. As per definition added to the Merriam-Webster dictionary only in 2018, cryptocurrency is any form of currency that exists purely in a digital form and has no central governance or an issuance body, for example, a government or a central bank. Instead, decentralized systems and cryptography are used to issue new cryptocurrencies, record transactions, and prevent fraud and counterfeit.

History of Digital Cash

In 1982, David Chaum, a famous cryptographer, conceptualized something he called e-cash, where digital money obtained from banks could be spent free of the central oversight. He later executed his ideas as DigiCash that survived till 1989. His research was invaluable to what we consider cryptocurrency today. It also became one of the pillars of the Cypherpunk movement, which came to life in the late 80s and 90s.

Cypherpunks were a group of people actively interested in cryptography, protection of individual privacy, and independence from the centralized systems and governments. The group converged around an anonymous email list where they exchanged ideas to push forward research in the fields of privacy-technology and cryptography. It is widely accepted that their conversations and experiments gave rise to the concept of blockchain and Bitcoin currency as we know them today.

Bitcoin Then and Now

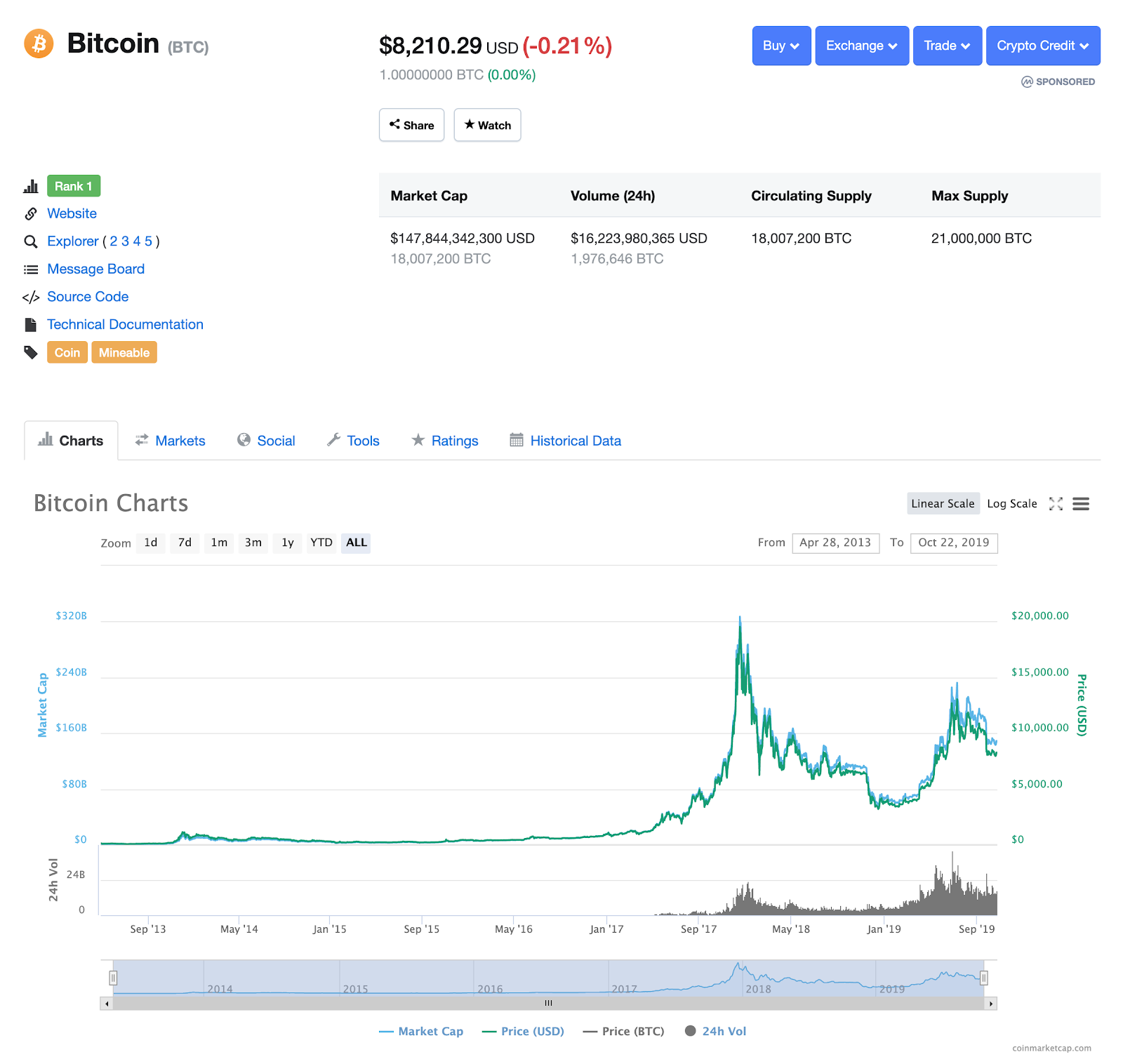

In 2008, a famous Bitcoin white paper was released by an entity or a group calling themselves Satoshi Nakamoto. The white paper outlined a new technology and the ideology behind the cryptocurrency. Bitcoin was formed as a ‘peer-to-peer electronic cash system’ independent of banks and governments, managed by a decentralized network of computers called nodes. Anyone could set up a node by downloading specific software and joining the network. In the following 11 years later, Bitcoin grew to a $147billion market cap. At its peak value in Dec 2017, each Bitcoin was worth over $20k. Currently, in a bear market, the value oscillates around $8,2k, but many speculate that the coin has only begun its climb.

How Cryptocurrencies Work

As per definitions, cryptocurrencies require decentralized systems and cryptography to take on the role usually reserved for banks and governing bodies. The system is designed to control and incentivize the execution of valid payment transactions and the issuance of new coins. There can be different ways to create such a system. Most, but not all, cryptocurrencies rely on the underlying blockchain technology. A distributed peer-2-peer network of nodes executes payments and puts the coin’s ownership records onto the blockchain. Examples of blockchain-based cryptocurrencies include Bitcoin, Ethereum, or EOS. There are also cryptocurrencies that don’t use blockchain, for example, IOTA.

Blockchain in a Nutshell

Most cryptocurrencies, including Bitcoin, rely on the blockchain technology. Blockchain is essentially a chain of digital blocks, tied to each other in a specific sequence. Like a folder in a database, each block contains data. For the cryptocurrency use case, blockchain carries records of financial transactions and proof of ownership of the crypto coins or other assets. It’s one of the reasons why blockchain is often referred to as a digital ledger.

The Distributed Ledger Technology

The blockchain technology is often called DLT for distributed ledger technology. Financial ledgers contain proofs of ownership and transaction information. Traditionally, they need to be validated by central authorities, which is both expensive and time-consuming. They also can be tampered with and prone to human-errors. Records stored on the blockchain are safer from both outside and inside influence because they are immutable, timestamped, and distributed.

- The benefits and methods for the timestamping of digital records have first been described by Haber and Stornetta in a groundbreaking paper from 1991. Accurate timestamping is vital for financial records. It allows us to track the history of the ownership of the asset.

- Immutability means no-one can change the records stored in the blocks. Thanks to hashing algorithms used in cryptography, each new block in the chain contains a digital fingerprint called a hash. Every block also carries the digital fingerprint of a previous block. Any changes in the data in a block would produce a completely different hash, and the altered block would stand out from the chain.

- Finally, digital blockchain ledgers are distributed, meaning a copy of the records is stored on many computers worldwide (on a distributed peer-2-peer network). It makes the data more secure from cyber-attacks and data loss, which happens for centralized systems with simple points of failure. That’s why we often refer to blockchain technology as DLT (Distributed Ledger Technology).

Who Makes Crypto Work?

Blockchain technology allows us to send money to our peers easily. But if banks are not involved, who checks if the payments are correct? Who puts the records on the blockchain?

The validation of the transactions happens thanks to the so-called consensus mechanism. Before any transaction ends up in the block, a majority of nodes have to agree that the payment is correct and valid. Each blockchain uses a different method to reach such a consensus. Various game theory principles and incentives are used to make the network participants play by the rules and agree on the actual truth.

Bitcoin and the majority of other cryptocurrencies use Proof-of-Work (PoW). In PoW, the nodes use software and computing power to solve complex mathematical problems. The work they perform allows them to validate transactions and add new blocks to the chain in exchange for fees. Some cryptocurrencies are testing alternative consensus algorithms, such as Proof-of-Stake and or decentralized voting mechanisms, to make sure the records are correct. In every case, the technology, together with predefined algorithms and social engineering, help the network stay functional.

Coin and Token Issuance

Depending on the case, the total number of coins can be set by the creators from the very beginning, or it can be unlimited. Bitcoin’s total number has been capped at 21 million coins, and the ‘new’ coins are discovered in the process of mining through Proof-of-Work. Ethereum’s total supply has not been capped, so, in theory, the new coins could be minted indefinitely. In each situation, the rules and methods to introduce new coins into the system are defined by the technology and its governance.

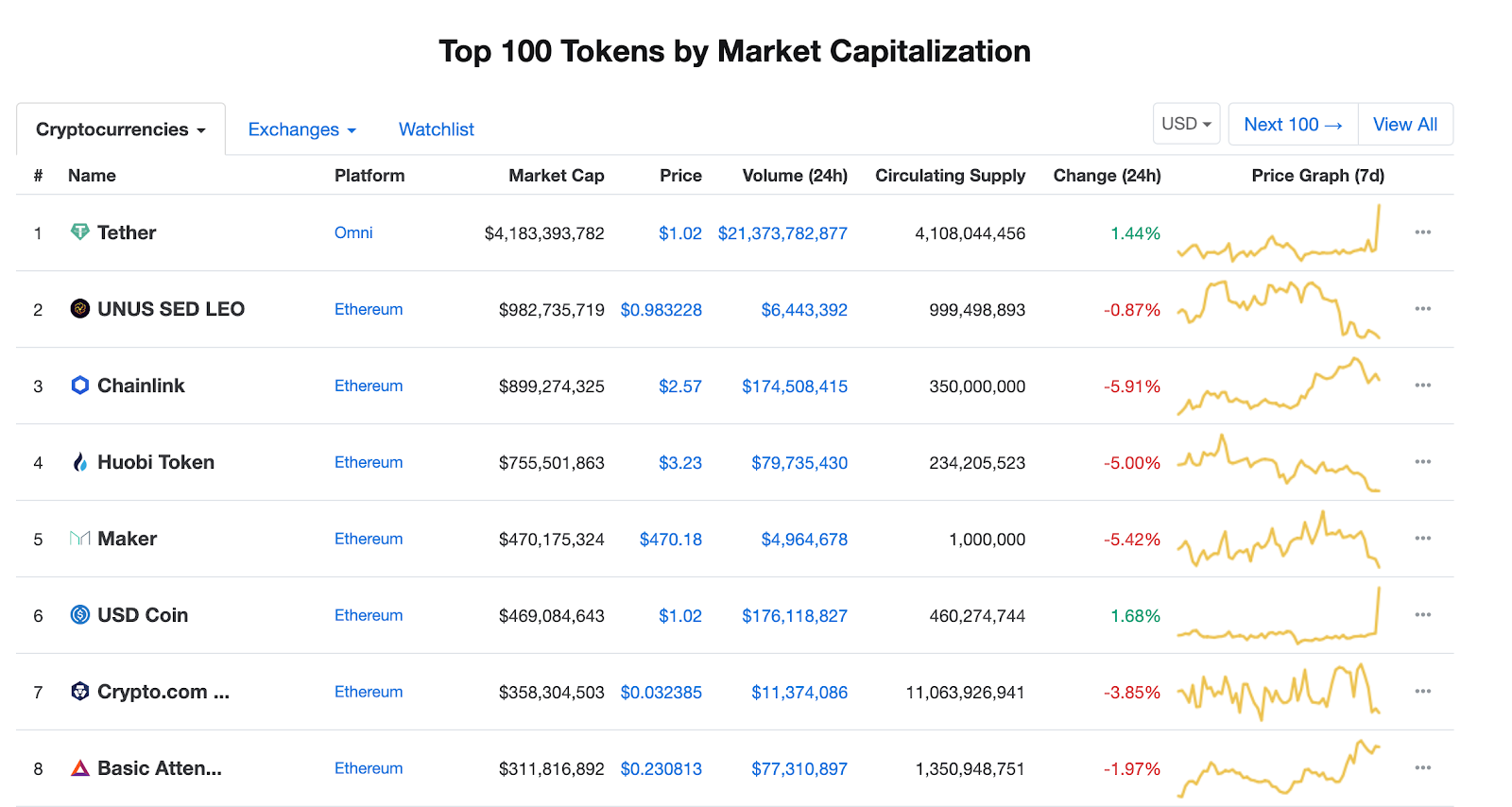

It’s worth mentioning that cryptocurrencies or cryptocurrency coins are not the same as crypto tokens. Tokens are digital assets that can be issued through smart contracts on the blockchains adapted to the token issuance, such as, Ethereum and Neo. Tokens usually represent some value like a utility, private equity, a real-world asset, a security token or a financial instrument. Successful tokens have large market caps and are traded on cryptocurrency exchanges alongside the coins.

Disclaimer: The opinion expressed here is not investment advice – it is provided for informational purposes only. It does not necessarily reflect the opinion of EGG Finance. Every investment and all trading involves risk, so you should always perform your own research prior to making decisions. We do not recommend investing money you cannot afford to lose.